As extreme weather events and climate change increasingly captures the attention of homebuyers in the U.S., a question comes to the forefront: to what extent does climate risk impact home prices?

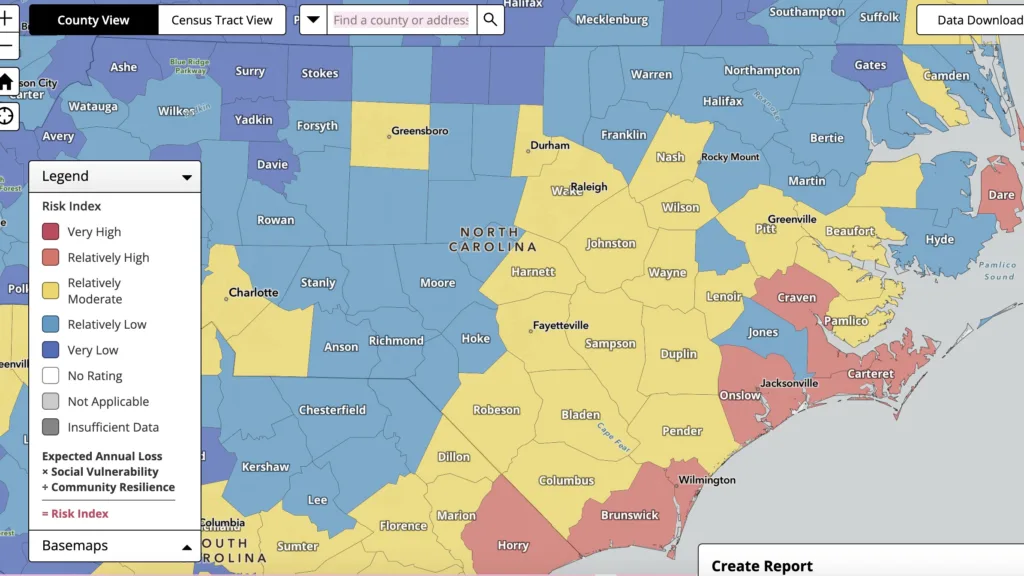

To answer this question we looked at the relationship between ZIP codes with the fastest-growing property values and the level of risk in corresponding census tracts, using data from the Federal Emergency Management Agency (FEMA)’s National Risk Index. We looked at this relationship in Florida, California, North Carolina, and Arizona.

It might seem intuitive that safety concerns and home insurance premiums, sharply rising over the last 30 years, would put downward pressure on home prices in high-risk areas throughout the country. But our research revealed that this was only part of the story. While markets like Arizona show much slower growth in high-risk areas, the exact opposite was true in Florida.

Research Methodology

- We used the median home price by ZIP code of all homes sold in Florida, California, North Carolina, and Arizona over the last three years. We designated markets that grew 2x the rate of the state as “Hot Markets.”

- We overlaid this data with FEMA’s National Risk Index (based on the corresponding census tract) to see how hot markets line up with climate risk levels, from very low to very high.

- Then we analyzed the patterns: Are the fastest-growing markets in safer, low-risk areas, or in zones more prone to weather-related threats?

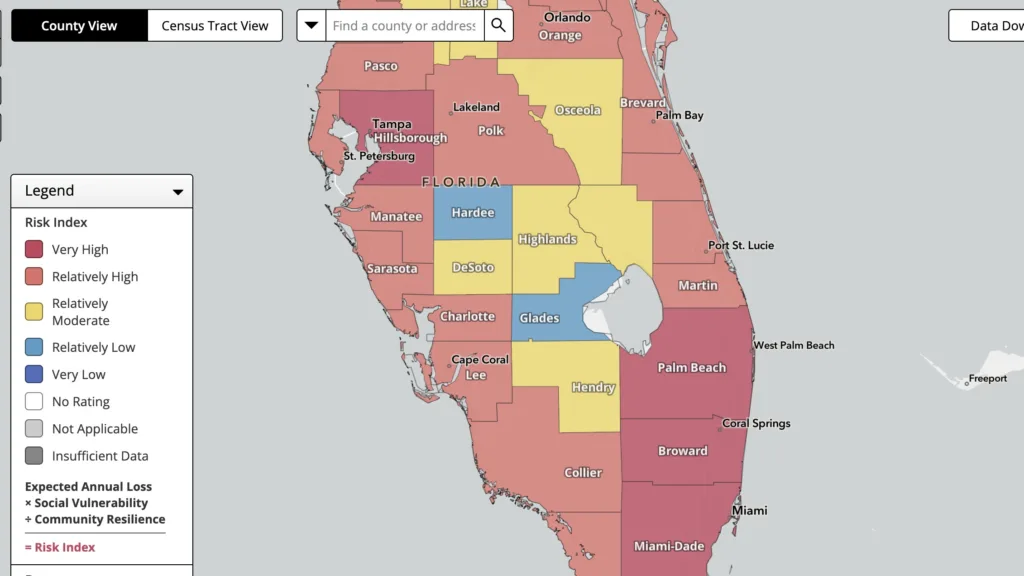

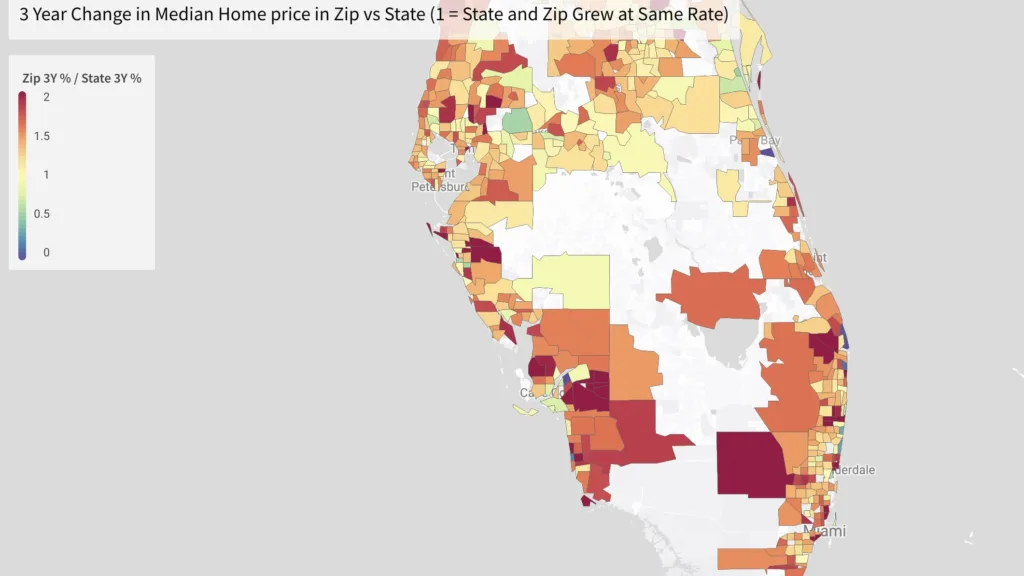

Florida: climate risk doesn’t deter

In Florida, “hot markets”—areas where the median home price grew at twice the rate of the rest of the state—are overwhelmingly in high-risk zones.

Buyers in these markets are 6x more likely to purchase in “relatively high” or “very high” environmental risk areas. In fact, 55% of Florida’s hot markets fall into high-risk categories, compared to just 9% in low or very low-risk areas. This growth underscores what McKinsey & Company describes as a potential gap in climate intelligence—buyers are prioritizing lifestyle amenities over long-term climate risks, which could lead to an eventual recalibration of property values in these high-risk zones.

Take a look at the Pembroke Pines area, just south of Fort Lauderdale. Here home prices have been increasing 2.5X faster than the rest of the state, yet it falls in a relatively high climate risk area due to changes of hurricanes and flooding. Beautiful beaches and high quality schools allow buyers to overlook the potential risks, along with seasonal owners who might not need to brave extreme weather outside hurricane season.

We see similar findings in desirable areas of Tampa, such as the Davis Island and Hyde Park neighborhoods. This too comes with relatively high climate risk, yet growth outpacing the rest of the state by more than double.

And parts of Miami, such as the Coral Gables neighborhood, is outpacing the state of Florida at a 1.5X rate, and is in a relatively high risk area.

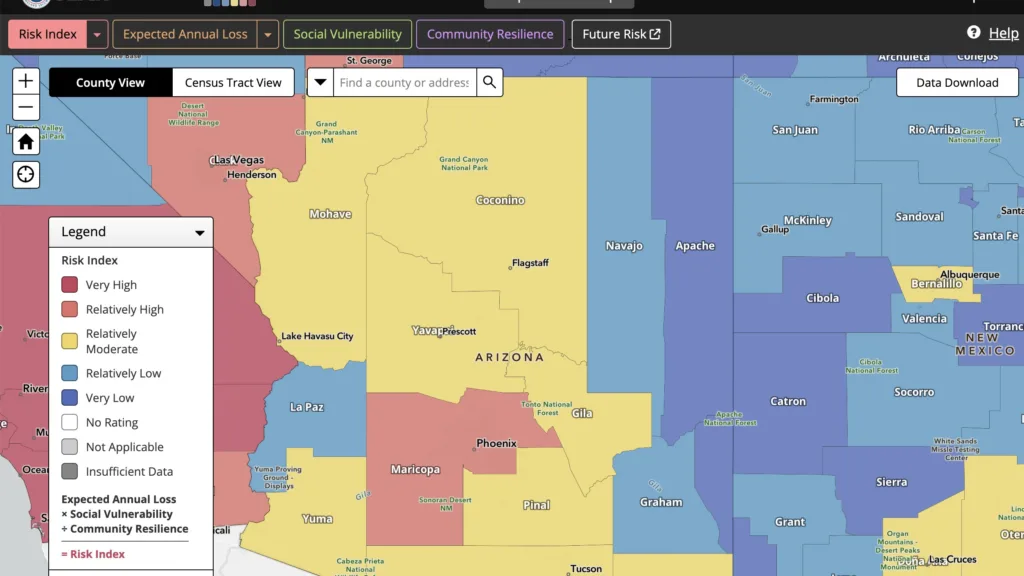

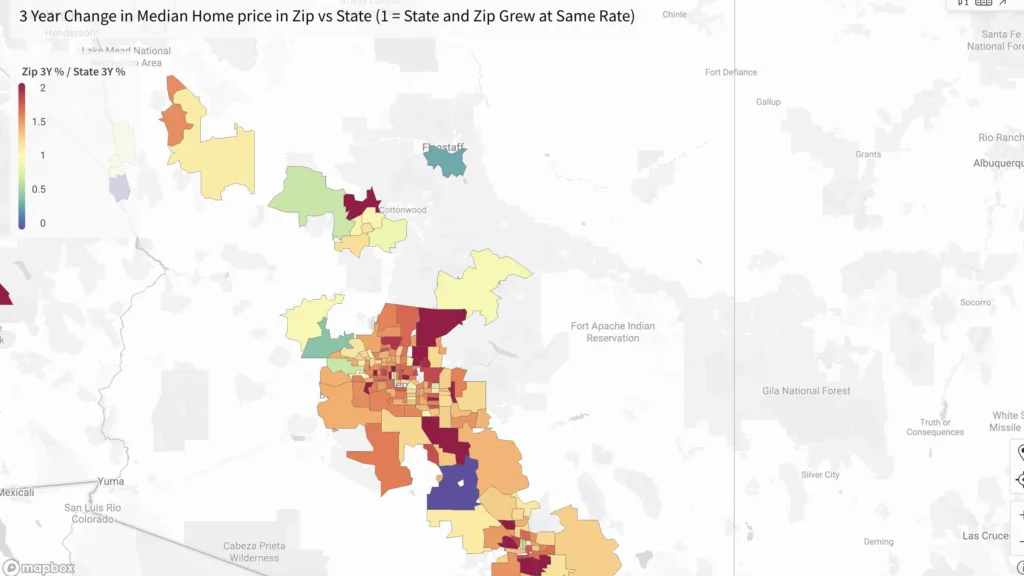

Arizona: fastest-growing markets concentrated in low risk areas

Rising prices in these areas signal a disconnect between what buyers want and the real Arizona’s real estate market demonstrates a clear relationship between climate risk and property value growth, with only 5% of AZ’s fastest-growing markets in high climate risk zones, and 91% in low climate risk areas. This data highlights how climate resilience, or the adverse costs of insurance for these homes, may have become a factor for homebuyers and put downward pressure on property value growth over the last three years.

For example, Scottsdale, a low-risk area, is growing 2.5x faster than the state average. Conversely, Prescott, a relatively high-risk area, is growing slower than the state average.

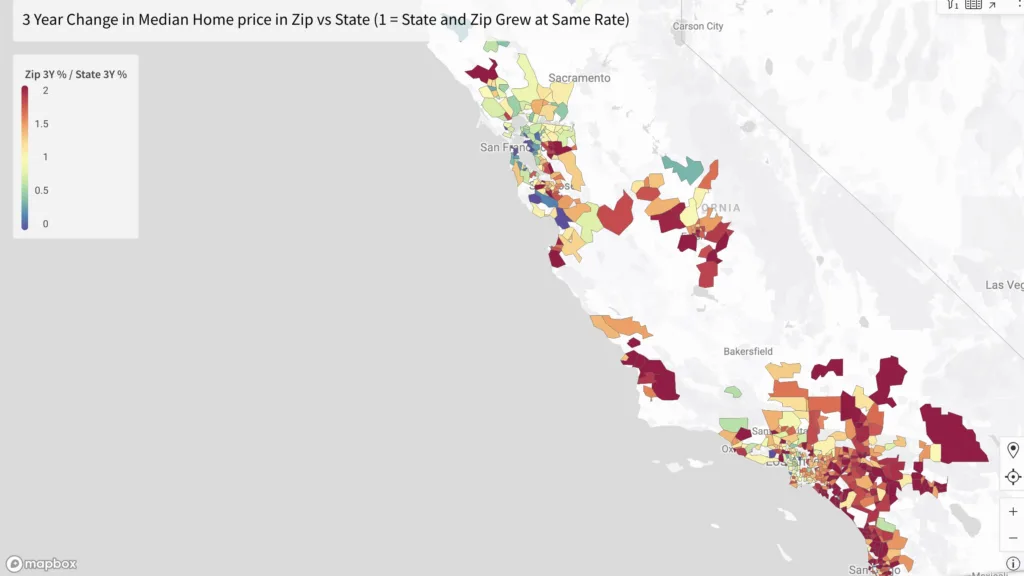

California: buyers forced to negotiate climate risk and affordability

California tells a more balanced story. While 36% of hot markets are in low-risk zones, the remaining markets are split between moderate (35%) and high-risk (29%) areas. In a state where housing inventory is tight, and the median home prices are almost double Florida’s, Arizona’s and North Carolina’s, buyers are still willing to venture into higher-risk areas like wildfire zones, but lower-risk areas remain slightly more attractive overall. Homes in high climate risk areas are growing at a slower rate, overall, compared to low-risk zones.

In Oakland/Emeryville, a high-risk area for climate disaster, the median home price has dipped compared to the state average rate of growth, while Fresno (a low-risk zone) home prices are growing 2.5x faster than the state average.

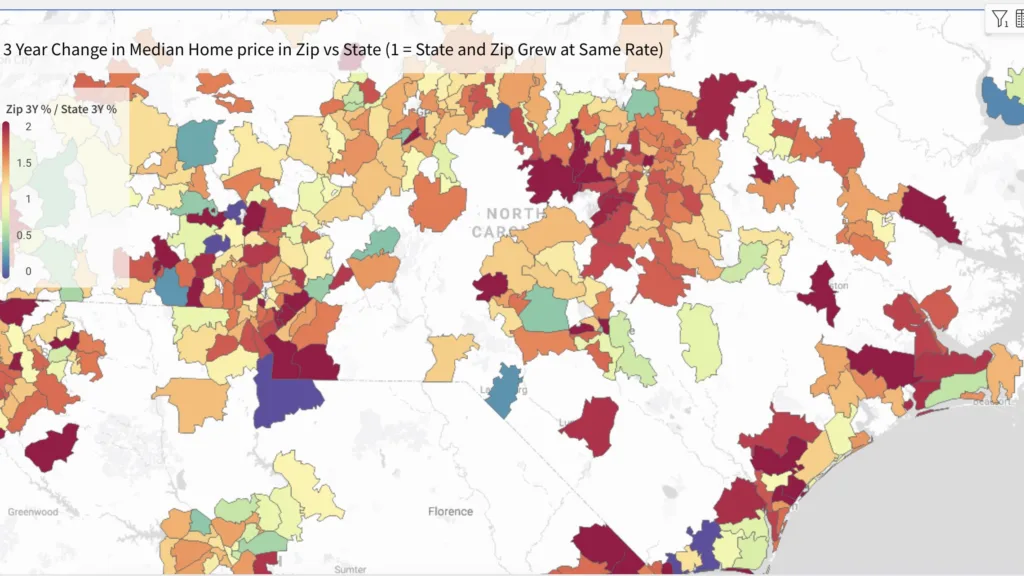

North Carolina: fastest-growing markets are in low risk areas

While overall home value growth is balanced between high and low risk areas in NC, the vast majority of North Carolina’s highest-growth markets are in low climate risk areas at 73%, with 18% in high risk areas. This trend is exemplified by the strong price growth in Charlotte’s 28209 ZIP code, a low-risk area that attracts buyers seeking safety and proximity to economic hubs.

In contrast, Brunswick County, a high-risk coastal region is experiencing slower growth compared to the state average. This lag may be attributed to elevated homeowners insurance premiums, which are influenced by the area’s increased susceptibility to hurricanes and flooding. According to MoneyGeek, Wilmington, a city near Brunswick County with similar coastal risk factors, has an average annual premium of $9,387 for a policy with $250,000 in dwelling coverage. In comparison, Charlotte’s average annual premium for the same coverage amount is approximately $1,781.

Regardless of where homebuyers live in North Carolina, homeowners’ insurance premiums are on the rise. While a 42% rate increase was initially proposed, negotiations resulted in a more gradual increase of approximately 15%, phased over 2025 and 2026. Insurers and the North Carolina Rate Bureau point to rising claim costs from extreme weather events, like hurricanes and flooding, as major drivers behind the hikes. Coastal areas face the highest risks, with repeated storms driving up both claims and recovery costs statewide.

Conclusion: insurance costs as a window into climate risk

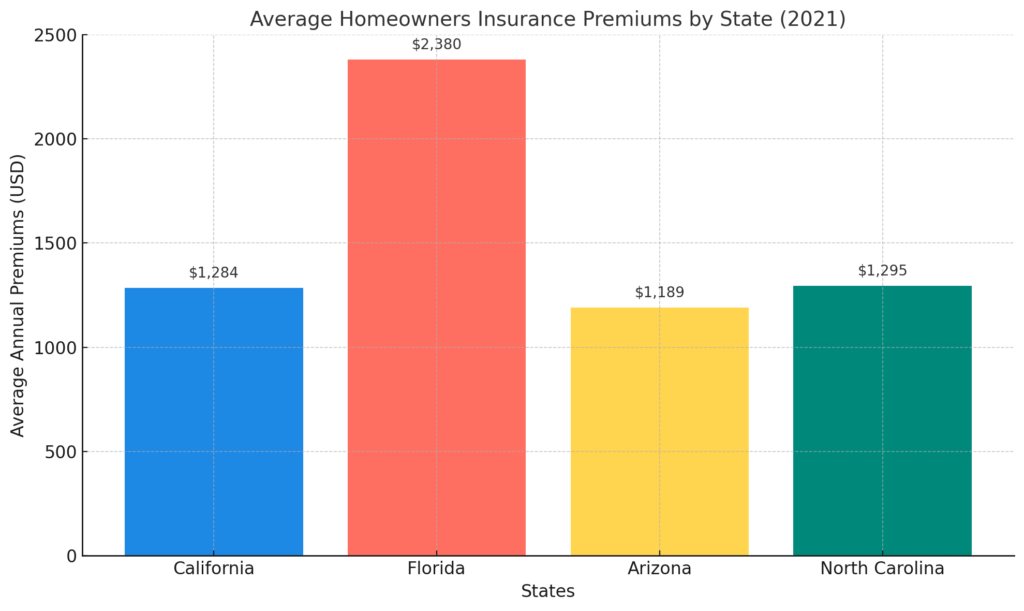

Sourced from The NAIC Homeowner’s Insurance Report (2021)

Insurance premiums give us a clear lens into how climate risks are reshaping the housing market. Whether it’s California’s wildfires, Florida’s hurricanes, Arizona’s heatwaves, or North Carolina’s flooding, these costs are becoming an increasingly significant factor in homebuyer decisions.

In Florida, buyers are heavily prioritizing high-risk areas despite the highest insurance premiums in the nation. In contrast, Arizona buyers overwhelmingly avoid high-risk areas, with just 5% of hot markets in these zones. North Carolina and California sit somewhere in between, balancing affordability and resilience as key considerations.

While climate risk hasn’t yet caused a dramatic shift in property values nationwide, it’s increasingly influencing buyer preferences—especially in markets with more options. These dynamics suggest that, as climate risks grow more tangible, buyers and investors will need to weigh lifestyle, affordability, and resilience more carefully than ever.

If you’re ready to start your journey to homeownership, get pre approved with Tomo Mortgage today.