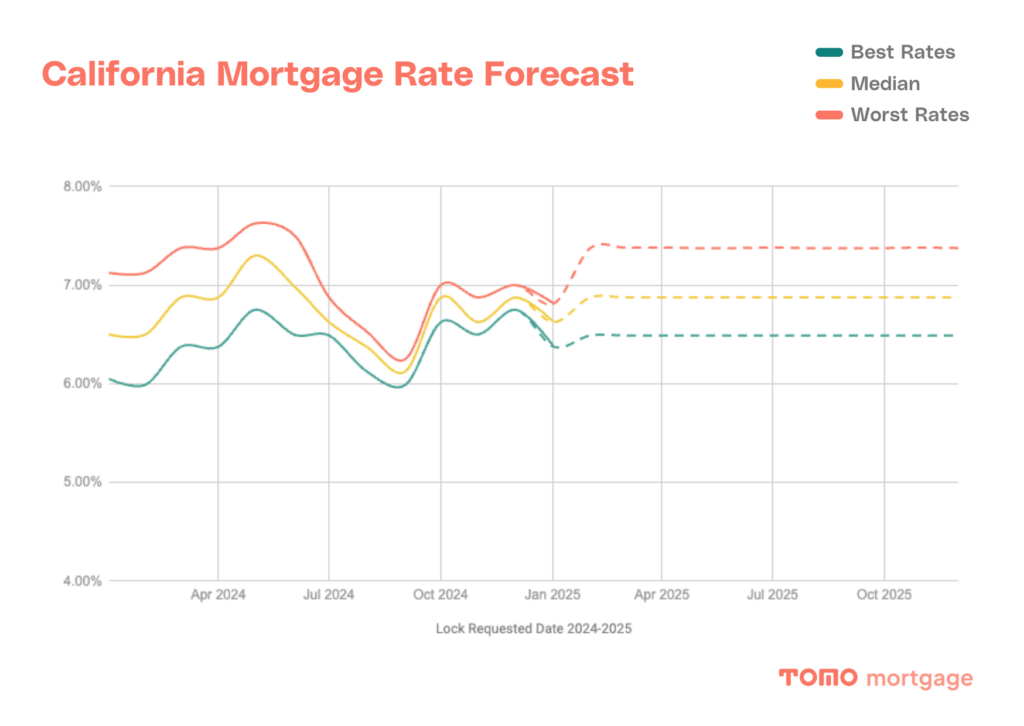

The chart above shows real interest rates locked for 30-year conventional loans in California for people with great credit (FICO score of 740+) by over 1,000 different lenders. The dotted line is our projected forecast for 2025, with rates looking like they’ll hold pretty steady nationally around 6.875% at the wrap of each quarter.

What is a good interest rate for home buyers in San Francisco right now

With home prices high, even a slight dip in interest rates can be a meaningful reduction in monthly payment.

If you’re looking for a home in Oakland and have good credit and sufficient income (a FICO credit score between 720 and 740), a typical buyer could target less than 6.63% interest rate and a good rate is around 6.5%.

Will interest rates go down in 2025?

For 2025, the market consensus is forecasting a slight drop in mortgage rates, from nearly 7% today to 6.5% by the end of the year. The Federal Reserve is signaling two rate cuts, but it’s important to remember that the Fed does not directly control mortgage rates.

At Tomo Mortgage, we believe the market is overly optimistic in its mortgage rate forecast and expect rates to end the year close to where they are now: 6.875%.

Key factors driving rates in 2025:

- The labor market: the labor market will continue to drive inflation outcomes and influence Fed policy. So far, it shows no signs of slowing down.

- Fiscal and regulatory policy: fiscal and regulatory actions will play a larger role in shaping mortgage rates than the Fed’s monetary policy. Key areas we are monitoring include:

- The prospect of mass deportations: this could tighten a labor force that has just returned to balance.

- The effect of tariffs: tariffs are inherently inflationary.

- The potential exit of Fannie Mae and Freddie Mac from conservatorship: this remains the largest wildcard outside the macroeconomy.

The odds of seeing mortgage rates dip into the 6s are not in favor. The latest Freddie Mac mortgage survey showed 30-year fixed mortgage rates at 6.91%. Historically, the odds of a drop of 0.91% or more from the first week of the year are slim—only about 25% of the time (13 out of 53 years) has this happened. Moreover, the risks for rates remain to the upside.

Check out today’s rates here

What might cause rates to increase or decrease this week?

Similar to last week, the back half of this week will have the most significant economic data. GDP and Jobless claims is released Thursday, and the most impactful release, PCE (which is the Fed’s preferred inflation gauge) is released on Friday. Here’s what to watch:

Q4 GDP (Thurs – 8:30am) GDP is the broadest and highest level measure of economic activity, but it is also significantly lagged relative to other measures of economic activity and employment. Economists predict a slowing of GDP from 3.1% to 2.3%, however economists have been predicting a GDP slowdown for successive quarters in expectation that higher interest rates will slow down growth. They have continued to underestimate the potential of the US Economy.

Weekly Jobless Claims (Thurs – 8:30am) While this is weekly data rather than monthly, and less impactful on a week-to-week basis, the weekly claims still are a signal of labor market strength/weakness. In recent months this release has trended closer to 220,000 than 200,000 indicating a gradual weakening of the labor market. Economists forecast 220,000 this week, in line with the previous week. Be on the lookout for a significant break above or below 220k. Small deviations will not move the market.

January Personal Consumption Expenditures (PCE) (Fri – 8:30am) This is the inflation measure that the Fed refers to when targeting “2%.” Core, ex-food and fuel, is expected to accelerate from .2% to .3%, and for the year the PCE is well above the target of 2% and remains “stuck.” Expect higher interest rates to continue provided this measure stays elevated and the job market remains relatively healthy.

Next: Calculate Personalized Rates