What is a down payment?

A down payment on a house is the upfront cash you put down when you buy a home. It reduces the amount you need to borrow, for example: if you buy a $445,000 home, and you put a $25,000 down payment down on it (which is putting about 5.6% down) you would then typically take out a mortgage for $420,000.

Saving for a down payment is one of the biggest barriers people face when it comes to buying a home—you might be able to afford the monthly mortgage payment, for example, but you might not have enough in the back to get the home in the first place.

But there’s a lot of confusion and misunderstanding about down payments and what’s better or worse for you financially in the long run. So, we’d like to debunk some myths and make sure you’re ready to make the right decision.

What percent should I put down for my down payment?

The simple answer: if you can afford 3% or 5%, it’s better to buy sooner than waiting for 20%.

Conventional wisdom from 50 years ago was that you needed to put 20% down. That was when homes were much more affordable, incomes were comparatively higher, and people were able to buy much younger. Your parents or earlier generations (and social media) perpetuates this myth today. But most first time home buyers put down between 3% and 8%.

In general, the more money or higher percent you put down for your down payment, the less interest over time and might even get better loan terms for your mortgage. If you put 20% or more down on a home using a conventional loan, you can avoid paying PMI (private mortgage insurance) which can add up over the course of a loan, as it most often falls between 0.5 and 1.5% of the loan amount per year. Once you pay your mortgage down so that you have 20% equity in your home, you can stop paying private mortgage insurance. If you go with an FHA loan you won’t have to pay PMI but you will have to pay a MIP (Mortgage Insurance Premiums)

To paint a picture of how this payment will add up, for a $300,000 loan, PMI might cost between $1,500 and $4,500 annually, which translates to $125 to $375 per month, and if you pay that for 8 years before selling or refinancing your home, that would add up to around $12,000-$36,000. Yikes!

But that’s not the full story. Saving for a down payment can be difficult and time consuming. Depending on where you live, you might have to save for 10+ years to get enough money to cover 20% down. And if you are renting while you save, it can be far more advantageous to begin paying your money towards your financial future as soon as you can. If that looks like a smaller percentage in a down payment, no sweat! (explore our guide on if it is better to rent or buy a home).

Is it better to put 3% down or 20% down?

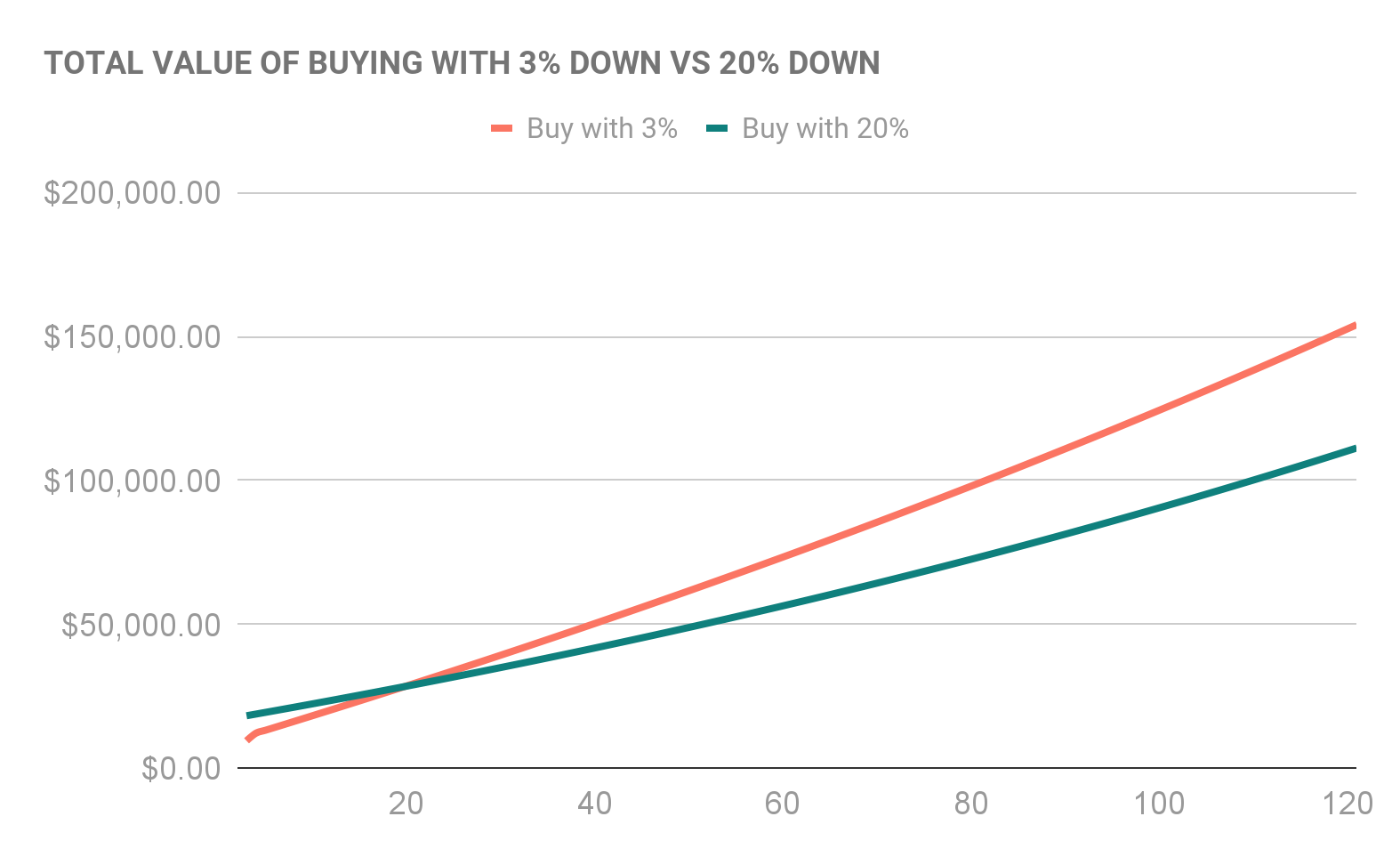

Let’s say you want to buy a $300,000 home. You make $100,000 per year and have $17,700 in savings, which gives you JUST enough to cover the 3% down payment ($9,000) and the estimated closing costs ($8,700). You currently pay $2,500 for rent and plan to save 10% from every paycheck. We’ll assume you’re good at your job and get regular raises (5% per year), pay for insurance, etc. And, we’ll assume that it’s more expensive to own a home in general (i.e., you have to pay for repairs, etc., at a typical 1% of the home value per year). There’s also a standard rent price increase each year (3.18%). Real world situation.

So, let’s look at these two scenarios over the next 10 years.

If you buy right away at 3%, after 10 years, you will have made $44,000 more than the person who tried to wait to save 20%.

Now, you may have to spend more on mortgage insurance in the 3% scenario. But at the end of the day you own a home and that home (over the long run, pretty reliably) will gain much more in total value than what you could gain through your savings alone. At the end of 30 years, that $300k home will be worth roughly $8.1 million. And during that 10 years you could invest in property improvements, refinance to lower your monthly payments (while the renter has little control), and be in a better financial position to upgrade into a better home.

If you wait for 20% down, you still don’t own a home after 10 years. You’d need to wait 15 years before you’d have enough in the bank to buy.

What is the minimum down payment for a house?

You will need to save at least 3% of your total desired home price to put as your down payment. That is the minimum for a conventional loan, and the minimum downpayment for a FHA loan is 3.5%. If you’re a veteran who qualifies, you can also get a home with 0% down.

What is the typical down payment on a house?

The average down payment in the United States is around 8%. But if you look a bit deeper into this number, it ranges quite a bit between first and second time homebuyers, with the average down payment for a first time home buyer being 6% of the total purchase price and 17% of the purchase price for repeat buyers.

In Q1 of 2024, the median down payment across all buyers in the U.S. was $26,700, which is around 8% of the median purchase price of a home in that period which was around $335,500 (according to Real Estate Data provider Atom).

What is a good down payment for a house?

A good down payment balances affordability with long-term financial health. While 20% is often recommended to avoid PMI (private mortgage insurance) and secure better loan terms, putting down less—like 10% or 5%—can help you step into homeownership sooner. Though you might face PMI costs initially, a smaller down payment allows you to start building equity in your home earlier.

What is down payment assistance?

If you’re hunting for down payment assistance, a good starting point is your state’s Housing Finance Agency (HFA) or local government—they often offer grants or loans that can really help. Nonprofits are also in the game, especially if you’re a first-time buyer.

For federal resources, HUD’s website lists local programs available by state. You can also use tools like DownPaymentResource.com to find and check your eligibility for assistance. Fannie Mae also has a great tool to help homebuyers find help with down payments.

Some state and city specific examples of down payment assistance programs include:

- San Francisco Down Payment Assistance Loan Program: Offers up to $500,000 in deferred down payment assistance for low- to moderate-income buyers, and

- Oakland CalHome Program: Provides a deferred loan up to $200,000 with 3% interest for first-time homebuyers

- Ohio Housing Finance Agency (OHFA) Programs for low income home buyers in the state of Ohio.

To qualify for these programs, you usually need to meet criteria such as a minimum credit score (around 620), income limits, and sometimes complete a homebuyer education course. It’s a good idea to start your research early to ensure you have enough time to apply.

Conclusion

Navigating the home-buying process can feel like a maze, but understanding down payments and how much you want and are able to put down on your home is a very tangible starting point.

Sure, everyone talks about that magic 20% down payment to avoid private mortgage insurance (PMI), but let’s be real—many people are getting into homes with way less, like 3% or even 3.5%.

So, when you’re thinking about how much to put down, consider your finances and the options available to you.

If you’re ready to start your journey to homeownership, get pre approved with Tomo Mortgage today.