OK, homes are really, really expensive right now. Affordability is rough in cities like Denver or Washington DC but even across the country home prices rose between 5% and even 10% in the last year. And that’s up from 15% or higher jumps in cities after the pandemic in 2021. And that rise doesn’t seem to be ending right now—Fannie Mae is forecasting a solid 6.1% increase by the end of 2024.

But, is there a decline on the horizon? Will prices drop next year? Will they drop anytime in the future? Both presidential candidates are talking about home affordability a lot, so maybe there’s some home there?

We don’t have a crystal ball but, overall, homes tend to grow in value over the long-run. And while you might remember the 2008 crash or little dips from city to city, the value of homes has shown steady growth, every year. Goldman Sachs Research has recently raised its forecast, predicting a 4.5% increase in U.S. home prices for 2024, followed by a 4.4% rise in 2025. Their outlook suggests a “slow grind” toward more balanced affordability over the next five years, driven by a mix of lower interest rates, rising incomes, and steady but tempered home price growth.

So if you’re hoping that a nice three-bedroom house in your area will drop by $50k over the next year, that probably isn’t going to happen. You’re more likely to see that same home sell for $50k more next year.

So, what’s keeping home prices so high?

1. Housing Inventory

The housing market is dealing with historically low levels of available homes, and it’s not keeping up with demand. The population of homebuyers is growing faster than new homes are being built, while smaller households (e.g., empty nesters holding onto large family homes) are further limiting available inventory for first-time buyers.

The Facts:

- The U.S. population is growing by 1.8 million people and 2 million households every year.

- However, the country is only adding 1.6 million new homes annually, meaning 400,000 more families each year are left without the opportunity to buy.

Over time, this imbalance has created a significant shortfall. Economists estimate that pent-up demand for new homes is between 1.5 and 3.8 million.

2. Strong Demand for Homes

Despite rising prices, demand for homes remains high. People are still eager to buy, especially with a growing population and increasing household formations.

3. New Builds Lagging Behind

Construction simply isn’t keeping pace with the strong demand for homes. The limited number of new builds exacerbates the inventory shortage, leaving many prospective buyers out of the market.

4. Investor Purchases

Another factor putting pressure on the housing market is the role of investors. Many are buying up moderately priced homes, often turning them into Airbnb properties. This takes away from the already scarce inventory of starter homes, making it even harder for first-time buyers to find affordable options.

Even if high mortgage rates dampen some buyers’ enthusiasm (though rates may be dropping), the severe lack of supply is likely to prevent nationwide price declines anytime soon. While some specific markets might see minor dips, a broad home price crash seems unlikely according to most economists.

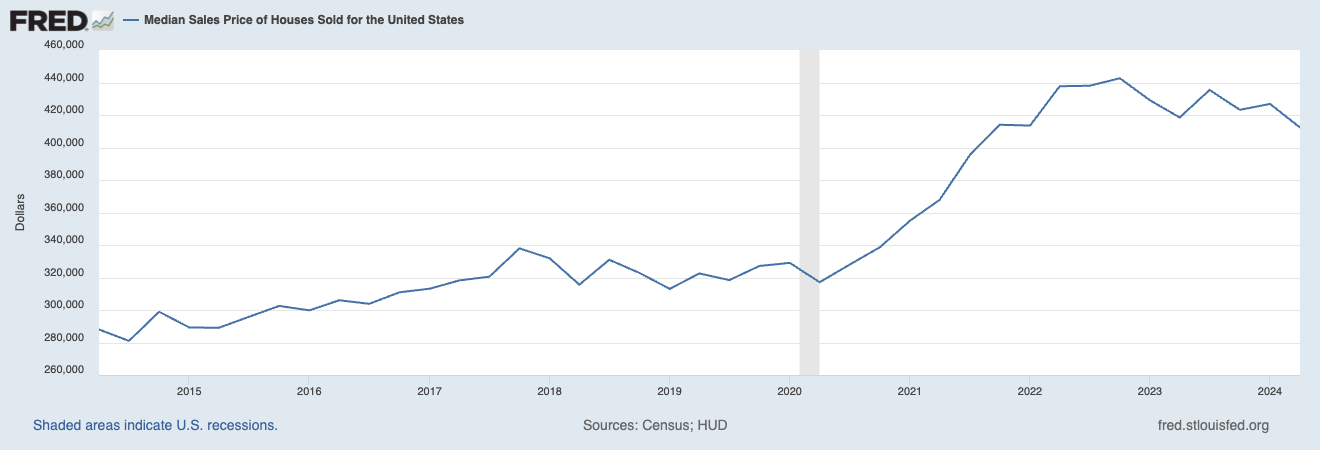

How much have home prices increased?

Take a look at this graph from FRED on the median home sales prices, year over year in the United States.

The housing market has seen significant movement over the past five years. From 2018 to 2023, median home prices jumped from around $300,000 to about $425,000—a substantial 41.7% increase. When looking at the broader period from 2017 to 2022, prices surged from roughly $270,000 to $400,000, marking a 48.1% rise.

Breaking it down further, in 2022, the median home price was about $400,000, up from $350,000 in 2021—an increase of 14.3%. The latest data shows that from 2022 to 2023, the median price climbed from $400,000 to $425,000, reflecting a 6.25% rise. These numbers highlight ongoing strong demand and tight inventory driving the market, despite broader economic fluctuations.

When did home prices most recently drop?

Home prices most recently experienced a notable decline during the early days of the COVID-19 pandemic in 2020. This period saw a temporary slowdown in price growth due to market uncertainties and economic disruptions. However, this dip was short-lived.

After the initial drop, home prices rebounded quickly and began rising sharply. This surge was driven by low interest rates, increased demand, and supply chain issues affecting new home construction. By late 2020 and into 2021, home prices had reached record highs due to a competitive buyer’s market and ongoing low inventory.

How does a lack of homes play into increasing home prices?

The shortage of affordable homes has intensified competition among buyers and driven prices higher. In many urban areas, the supply of affordable homes is so limited that first-time buyers are often priced out. This situation creates a cycle where only those with significant wealth can afford homes, further widening the wealth gap.

If you’re ready to start your journey to homeownership, get pre approved with Tomo Mortgage today.