Here’s the scoop: Interest rates are always on the move, which can make it tricky to figure out the right time to lock in a mortgage rate or buy a home. Should you act now or wait for a better deal? This question might keep many of us up at night.

Truth is, the Fed works to keep rates fairly predictable. Their decisions on rate increases or cuts are forward-looking, aiming to smooth out the ups and downs of economic data, like changes in the labor market, so things stay relatively steady over time, and the amount of money you’d save or loose on your rate is typically pretty small when it comes to the day to day changes.

When you’re tracking mortgage rates, it’s helpful to see how both significant year-over-year changes and minor daily fluctuations impact your pockets.

For instance, the drop from 7.875% in fall 2023 to 6.625% in summer 2024 could save borrowers about $242 a month. But don’t get too caught up in the smaller daily rate changes. For example, a 0.15% increase—from 6.625% to 6.775%—would only add about $33 to your monthly payment and $7,000 over 30 years (and most people don’t keep their mortgage for more than 8 years anyways).

The Fed meets 8 times a year for their FOMC (Federal Open Market Committee) and following these meetings is when you may see larger rate cuts worth paying attention to. If the Fed cuts rates, mortgage rates will likely follow.

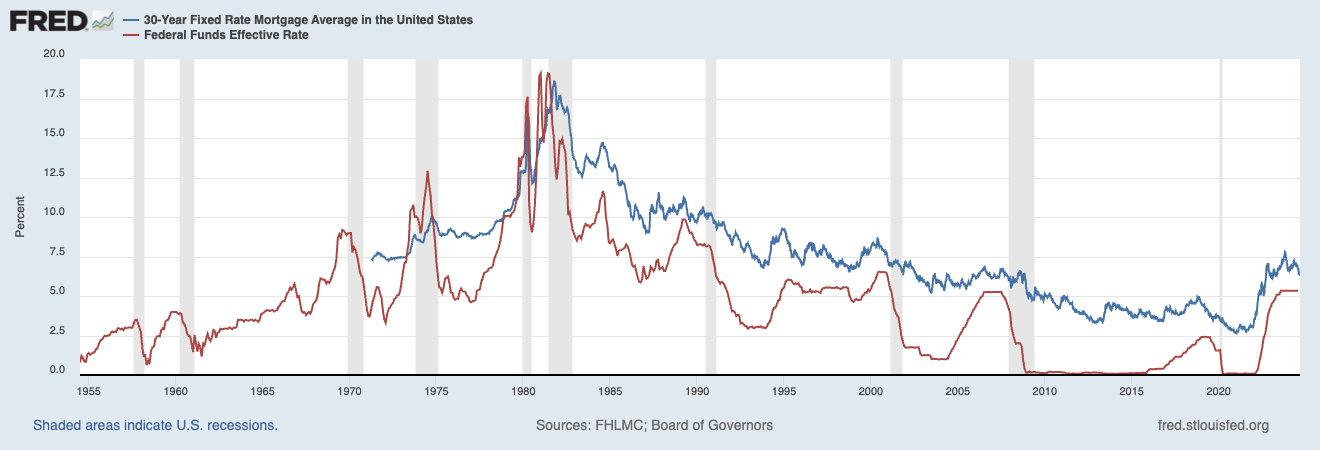

This graph illustrates the historical relationship between the Federal Funds Effective Rate and the 30-year fixed-rate mortgage average.

Check out our mortgage rate forecast for up to date insights and what it could mean for your home-buying journey.

2025 outlook

In 2025, the real impact of the Fed’s 2024 rate cuts will start to unfold. If the Fed’s strategy works— keeping inflation in check—mortgage rates might continue to decline. It is a safe guess to say rates will go down, but stay up to date to see how much and when.

Why are mortgage rates so high?

Mortgage rates increased primarily due to inflation and the Fed’s actions to manage it. In 2022 and 2023, the Fed raised interest rates significantly to combat inflation, which in turn pushed mortgage rates higher.

Economic factors like job growth and unemployment also influence the Fed’s interest rate decisions. After COVID-19, the Fed lowered rates to stimulate the economy, but as recovery took hold, supply and demand imbalances—exacerbated by supply chain issues and global events like the Russia-Ukraine conflict—drove prices up. To fight this inflation, the Fed started raising rates, they shared this video to break it down.

Why do interest rates change?

Credit Supply and Demand: Imagine interest rates are like the flow of water from a faucet. When lots of people want to borrow money (high demand) and there’s not enough credit available (low supply), it’s like trying to get water from a narrow faucet—there’s less water coming out, and it comes out faster (higher interest rates). When fewer people need to borrow money (low demand) and there’s plenty of credit available (high supply), it’s like having a wide-open faucet—more water flows out slowly (lower interest rates).

Government Actions: The Federal Reserve controls the faucet of borrowing money. If they want to make borrowing easier and cheaper, they turn the faucet wider (lower interest rates). If they want to make borrowing harder and more expensive, they turn the faucet narrower (higher interest rates). This adjustment helps manage how much borrowing and spending happens in the economy.

Why would the government want to make borrowing easier or more difficult?

The government, through the Federal Reserve, adjusts how easy or hard it is to borrow money to keep the economy stable. Here’s why:

Making borrowing easier: When the economy is struggling, like during a recession, the Federal Reserve might open the faucet wider (lower interest rates) to make borrowing cheaper. This encourages people and businesses to take out loans, spend more, and invest. The goal is to boost economic activity and help the economy recover. Imagine if you were trying to start a garden but needed more water to grow your plants. By making more water available, you help the garden flourish.

Making borrowing harder: When the economy is growing too quickly, leading to high inflation (prices rising fast), the Federal Reserve might turn the faucet down (raise interest rates) to make borrowing more expensive. This helps slow down spending and borrowing, which can cool off inflation and prevent the economy from overheating. It’s like reducing the water flow to keep your garden from flooding, ensuring the plants get just the right amount of water without causing problems.

In short, the government adjusts borrowing conditions to either stimulate the economy when it’s weak or slow it down when it’s too hot, aiming to keep everything balanced and stable.

Is it important to buy a home with a low interest rate?

Your interest rate will play a big role in the cost of your home loan over its lifespan, so being aware and trying to get the lowest rate you can is important. That being said, there’s a saying that you date the rate but you marry the home… Meaning that while your rate is a factor, it is temporary, as you can refinance your home loan once/if rates drop to get a lower interest rate. But if you pass up your dream home, it may not come around again. There is an element of risk involved, as there is no certain way to say when rates will drop, so while you are not married to your rate, you want to make sure you are comfortable paying it for the short term.

Waiting for slightly lower rates might not be worth it when you consider the other financial benefits of buying sooner. For instance, investing in real estate now allows you to start building equity and potentially benefit from property value appreciation. This can lead to a much greater financial upside than the $50 a month you might save from a lower interest rate. So, while it’s important to consider your rate, it’s also crucial to weigh the overall benefits of owning a home now versus waiting.

Conclusion

While it’s tempting to try to time the market and wait for the perfect interest rate, it’s crucial to remember that predicting these changes with precision is incredibly challenging. Instead of getting caught up in the fluctuations of daily or even yearly rate shifts, focus on what you can control: your readiness to buy a home when the opportunity arises.

Interest rates will ebb and flow, but the benefits of homeownership—such as building equity and potentially benefiting from property appreciation—are immediate and tangible. By purchasing a home when you’re financially prepared, you can start building equity and investing in your future. Waiting for slightly lower rates might not be worth missing out on a dream home or delaying your financial progress.

Remember, while you can always refinance your mortgage if rates drop in the future, you can’t always find the right home when you need it. So, rather than trying to game the system, make your move when it makes sense for you and your financial situation, and take advantage of the opportunities that come your way.

If you’re ready to start your journey to homeownership, get pre approved with Tomo Mortgage today.