You’re paying to borrow. When you take out a mortgage, you’re borrowing a large sum from the bank or lender. The interest rate is essentially their fee for lending you the money. It’s not just the amount you borrow (the principal) that you need to pay back—you’ll also owe interest. This interest is calculated as a percentage of the loan balance and is added to your monthly mortgage payment. The higher the interest rate, the more you’re paying in total over time. Even a small change in the interest rate can make a significant difference in the total amount you pay over the life of the loan.

How do interest rates affect my monthly mortgage payment?

Your interest rate has a direct impact on your monthly mortgage payment. The higher your rate, the more you’ll pay in interest each month. In the early years of the loan, most of your payment goes toward interest, not the principal. Over time, as you pay down the loan, more of your payment will go toward the principal. A higher interest rate can also limit how much house you can afford, as it increases your monthly payment and total cost over time. For example, a difference of just 1% in your interest rate can add up to tens of thousands of dollars over the life of a 30-year mortgage.

How can I get the best interest rate on my mortgage?

There’s about a million different factors that affect your specific interest rate on a loan. In fact, there’s a pretty good chance that no one, anywhere in the country, has the exact same financial profile as you do right now when you’re looking for a rate.

So, what makes the difference on a loan rate? If you have acceptable credit (anything about 580), and are looking at a fairly conventional loan situation (primary residence, single-family home, etc.), the difference in rates mostly comes down to the lender and “the market.”

Market conditions: Interest rates fluctuate based on economic factors like inflation, unemployment, and Federal Reserve policies. When inflation is high, interest rates often go up to slow down spending. The Federal Reserve can also influence rates by adjusting its benchmark rates, which impacts the cost of borrowing across the board. These market changes are out of your control, but they play a big role in the rates lenders offer.

The Lender: What is in your control is which lender you choose. There’s a HUGE difference between what lenders change the exact same person in the same situation. For example, we looked at thousands of loans that were locked in by different lenders (a good representative sample of the entire industry, including major banks and the biggest lenders in the U.S.). What we found is that the gap between the best rates and worst rates was upwards of $20,000. We also saw that 9 in 10 home buyers could have saved a lot of money by going with Tomo—$5,200 was the median savings.

Apart from these factors, you’ll want to make sure the loan itself is getting you the best terms. This means making sure you think through all your options, like whether you should use a little of the down payment to buy rate points. Shorter loan terms (like 15 years vs. 30 years) usually come with lower interest rates because the lender’s risk is reduced. However, shorter terms also mean higher monthly payments, even though you pay less interest overall.

Finally, there’s credit score—lenders look at your credit score to assess how risky it is to lend to you. A higher credit score signals you’re less of a risk, which can get you a lower interest rate. If your credit score is low, you’re likely to face a higher rate, costing you more in the long run.

What factors influence mortgage interest rates nationally?

Mortgage interest rates aren’t just influenced by your personal financial situation—they mirror some powerful market dynamics. Inflation and GDP growth are major players. When inflation surges, the Federal Reserve typically raises its rates to cool things down, and mortgage rates follow suit. This means as the Fed adjusts its rates, lenders align their mortgage rates accordingly to stay competitive and maintain their profit margins.

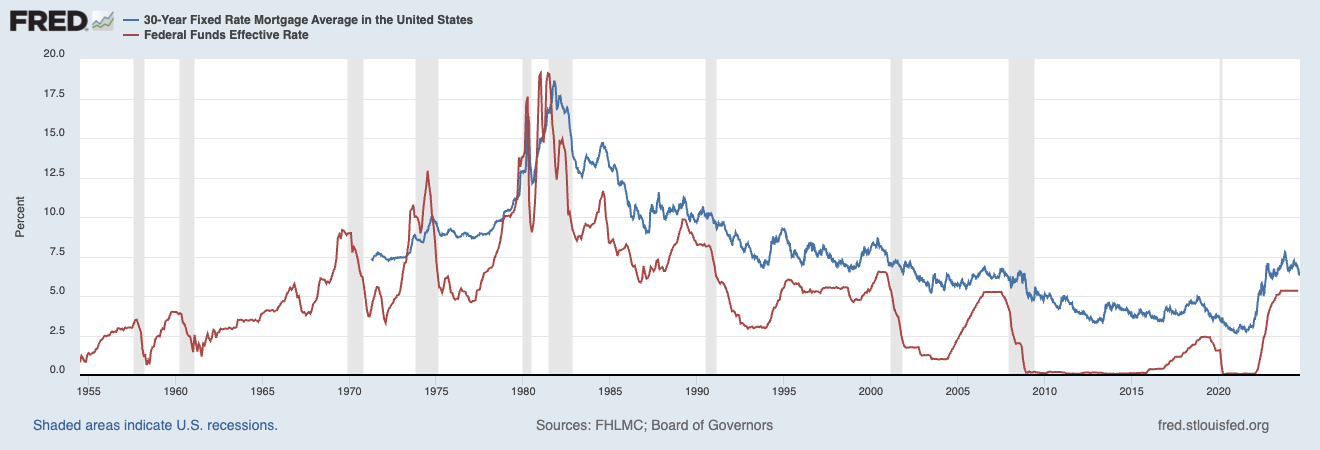

Here is a chart from FRED showing the Federal funds effective interest rate, and how the 30 year fixed mortgage rate mirrors it.

A booming economy also ramps up loan demand, which can push rates higher. Additionally, global events can shake things up. For instance, international instability might lead investors to flock to U.S. Treasuries for safety, impacting yields and, by extension, mortgage rates. Understanding these broader economic influences helps explain why mortgage rates fluctuate and how they reflect the economic landscape.

Are current interest rates expected to go up or down?

Rates have since started to drop since Summer 2024, and are forecasted to continue to decline for the rest of 2024 and into 2025. Check out our Interest rate forecast for interest rate predictions and upcoming events to look out for.

What does locking my rate mean?

Locking your mortgage rate is your way of grabbing a specific interest rate and holding onto it for a set period—usually 30 to 60 days, though some lenders offer different time frames. This move means you’re locking in that rate, no matter how the market shakes out during the lock period. If rates shoot up while your loan is in the works, you’re shielded from those hikes because your rate stays put.

This strategy gives you financial stability by locking in a clear picture of your future monthly payments, making your budget and financial planning a lot more predictable. It’s a smart move if the market is shaky or if rates are poised to climb. Securing a favorable rate now means you won’t get blindsided if rates rise before your mortgage closes.

On the flip side, if rates are high and anticipated to drop soon, waiting to lock your rate could be advantageous, because it would be a bummer to lock your rate to realize you could have saved significantly had you waited. Deciding whether or not to lock your rate is kind of like playing poker, you’re hedging your bets without fully knowing what the future holds.

Float Down Policy:

If you want more flexibility while locking your rate, some lenders offer a float down policy. This option lets you secure a lower interest rate if market rates drop after you’ve locked in your original rate but before your loan closes. It’s like having a “just-in-case” backup—if rates go up, you’re protected, but if they go down, the float down allows you to adjust and get the better rate. However, this option often comes with certain fees or conditions, such as how much rates need to fall before you can take advantage of it. So, while it gives you peace of mind, it’s important to weigh whether the cost of the float down is worth the potential savings.

How do interest rates differ between lenders?

Interest rates can differ significantly between lenders due to their unique operating models, cost structures, and risk management practices. At Tomo Mortgage, we offer some of the lowest rates in the industry, 0.48 points lower than the median rate nationally. This can result in savings of over $5,000 for many buyers.

We automate the behind-the-scenes stuff in a mortgage, which makes it cheaper to give loans, and then we pass that savings on to home buyers. By reducing costs through technology, we’re able to offer no fees and lower rates. As a result, 9 out of 10 people who choose Tomo Mortgage end up saving money on their mortgage.

How do rising interest rates impact home affordability?

Rising interest rates can shake up home affordability in a big way. When rates climb, so do your monthly mortgage payments. For example, if your rate bumps from 3.5% to 4.5%, a $300,000 loan could see its monthly payment spike by several hundred dollars. This squeeze on your budget might force you to rethink the size or location of your dream home.

But it’s not just about the monthly hit—higher rates mean you’re shelling out more in total over the life of the loan. Picture this: a 1% rate increase on a 30-year mortgage can add tens of thousands to your final bill. That’s a hefty chunk of change in interest alone.

Your purchasing power also takes a hit. With steeper rates, you might find you can’t afford as much house as you could with lower rates. Say you were eyeing a $400,000 property at 3.5%; with a rate bump to 4.5%, that could shrink your budget to around $350,000, altering what you can buy.

Now, you might think that as rates increase people might need to sell their home for less (or vice versa). So far, we haven’t seen that in the data. Home sellers have a price in mind and tend to stick to it, regardless of the mortgage cost, because it’s a competitive market regardless of the interest rates.

In a nutshell, rising rates mess with home affordability by jacking up monthly payments, inflating the total loan cost, and shrinking your buying power. This shift also plays into the broader housing market, so it’s smart to factor these changes into your home-buying strategy.

How is the APR different than the interest rate?

The interest rate tells you the cost of borrowing money, but the APR (annual percentage rate) gives you a more complete picture. APR includes the interest rate plus other fees and costs associated with the loan, like closing costs and loan origination fees. It’s the true cost of the mortgage over time. Comparing APRs, not just interest rates, can help you understand which loan is actually cheaper when you factor in all the costs. Lenders are required to disclose the APR, so pay attention to this number when shopping for a mortgage.

If you’re ready to start your journey to homeownership, get pre approved with Tomo Mortgage today.