Mortgage fees have climbed in recent years—but not evenly. New data from Tomo TrueRate shows that the largest mortgage lenders are driving the biggest increases in lender fees, far outpacing both inflation and smaller competitors.

The data reveals a growing pricing disparity that raises questions about how lender size influences cost—and how informed buyers can avoid overpaying.

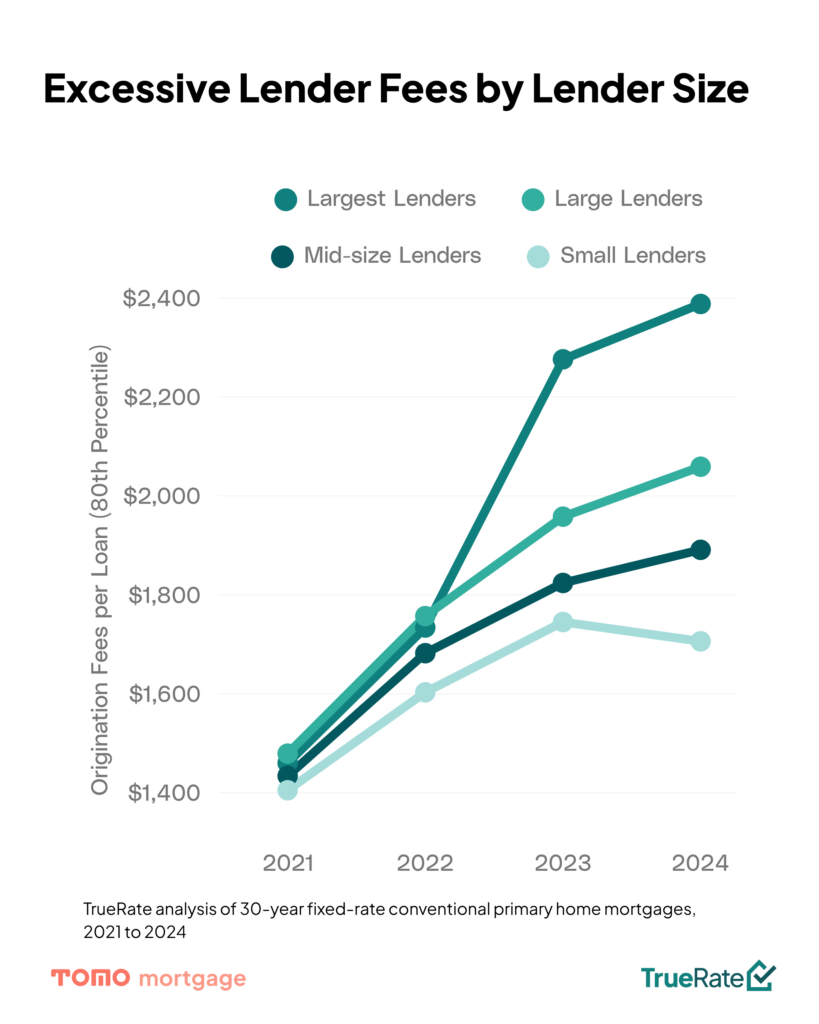

Big lenders, big fees

In 2021, excessive lender fees (80th percentile of fees from a single lender) were nearly identical across lender sizes. But as the refinance boom ended in 2022, the gap widened dramatically. Fees from the biggest lenders (originating over 5,000 loans per year) rose by a staggering 64%. By contrast, excessive fees from smaller lenders (200 to 500 purchase loans annually) grew 21.4%, which is consistent with the rate of inflation over the same period.

What are these fees for?

Most of these charges fall under Section A of your Loan Estimate, where lenders list their own origination fees. These can include line items like “underwriting,” “processing,” “application,” and sometimes even vague terms like “commitment” or “satisfaction” fees.

Unlike third-party costs (like appraisals or title insurance), Section A fees are entirely set by the lender—and they’re one of the biggest sources of variation in what buyers pay at closing. Two lenders offering the exact same interest rate can differ by thousands of dollars in fees.

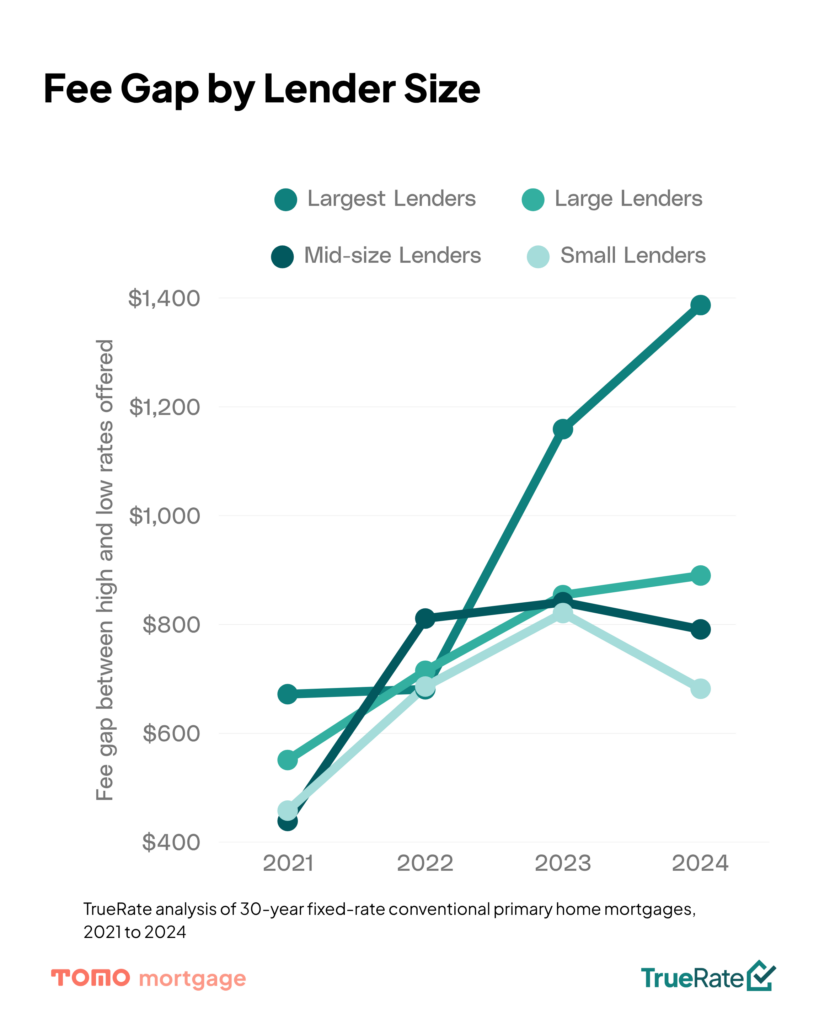

Negotiation room—or pricing strategy?

In 2024, large lenders charged an average high-end fee of $2,388—but the spread between their highest and lowest fees was $1,387, meaning some borrowers successfully negotiated their fees down to around $1,001.

Smaller lenders charged an average high fee of $1,706, with a narrower spread of $682, resulting in a negotiated fee of about $1,024.

This suggests that larger lenders are not charging more because they have to—they’re charging more because they can. Savvy buyers may recognize this and negotiate down. But many buyers, especially first-timers, may not know they even have that option—and end up shouldering the higher cost.

Why this matters for homebuyers

This growing disparity in mortgage fees underscores a critical point: lender choice matters. Two borrowers with the same financial profile could receive dramatically different fee structures depending on where they go—and how much they know to push back.

For some, that means savings. For others, it could mean paying thousands more at closing—just because they didn’t know they had a choice.

Want to see how your lender compares?